The 'Permis Ci' Matrix and its Structural Impact on Diplomatic Household Capital

As the summer diplomatic rotation approaches its peak across Geneva’s international district, hundreds of families holding Federal Department of Foreign Affairs (FDFA) Legitimation Cards are navigating their administrative onboarding. While the principal official’s legal status is securely ring-fenced by bilateral seat agreements and the Vienna Convention, an asymmetric compliance risk emerges when a trailing spouse chooses to enter the local Swiss labor market. Far from being a routine career step, transitioning from a derivative diplomatic status to a local economic actor triggers a structural transformation in the household's fiscal, social security, and insurance frameworks.

The Legal Mechanism of Status Transformation

Why does a local employment contract alter the foundational architecture of an international household? The core legal philosophy of diplomatic privilege is designed to insulate foreign officials from domestic civic burdens. However, the moment a dependent spouse signs a standard Swiss employment contract exceeding ten hours per week, the Canton of Geneva categorizes them as an active domestic economic agent. To bridge this legal gap without compromising the principal earner's status, the Swiss Federal Authorities implement a specific regulatory protocol:

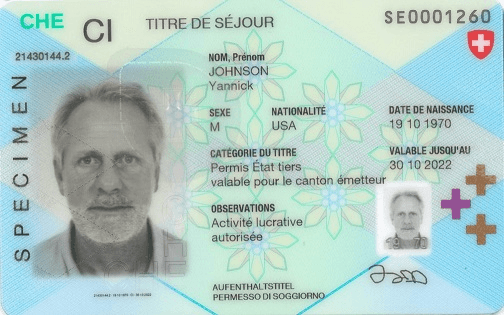

The OLEH Article 22 Protocol: Eligible family members must formally surrender their Legitimation Card to the Swiss Mission. In exchange, the Office Cantonal de la Population et des Migrations (OCPM) issues a Livret pour étranger Ci avec activité lucrative. This special permit guarantees un-contingented access to the Swiss labor market—exempting the holder from local worker quotas and priority rules—but systematically strips away all extraterritorial fiscal immunities for that specific local income.

The Fiscal Reality: The "Ménage Mixte" Conundrum

Once the Livret Ci is activated, the household enters what Swiss tax authorities define as a "Ménage Mixte" (Mixed Household). This creates a multi-layered tax environment that requires meticulous structural optimization to prevent unexpected liabilities:

1. Total Global Household Income (Exempt International Salary + Local Salary)

-Cantonal Fiscal Classification: Rate Progression Factor (Taux global de progression)

Administrative Mechanism: This cumulative figure is used solely by the Geneva -Tax Administration to calibrate the progressive tax bracket percentage. Crucially, the primary official’s diplomatic or institutional earnings remain entirely un-taxed; they are merely utilized as a benchmark to determine the tax rate applied to the spouse's income.

2. Spouse’s Local Swiss Salary (Permis Ci Earnings)

-Cantonal Fiscal Classification: Taxable Base (Assiette fiscale)

-Administrative Mechanism: This is the specific, isolated asset class subject to direct, monthly withholding tax (Impôt à la source). It is calculated using Geneva's standard tax scales and is automatically processed and deducted directly by the local Swiss employer.

For married couples, the initial tax withholding defaults to Barème C (double-income scale). If the structural distribution of income between the international salary and the local salary is unbalanced, the household faces significant upfront over-taxation. Mitigating this requires a formal adjustment request (Rectification) to be meticulously filed before March 31 of the subsequent fiscal year.

Barème C / Impôt à la source: Couples mariés disposant de deux revenus

-Direct Withholding (Impôt à la source): The spouse’s Swiss salary is subject to immediate monthly deductions by the employer based on Geneva’s specific withholding tables.

-The Progressive Bracket Catch: While the principal diplomat’s international salary remains strictly tax-exempt under international law, the cantonal tax administration utilizes the couple's combined global household income to determine the progressive tax rate bracket applied to the spouse's local Swiss earnings.

-Barème C Implication: For married couples, the default withholding utilizes Barème C (two-income household scale). If the actual income distribution between the spouses diverges significantly from the baseline assumptions of this scale, an adjustment (Rectification) must be filed before March 31 of the subsequent year to recapture overpaid taxes.

Asymmetric Social Security Footprints

Simultaneously, the social security framework of the household splits into two entirely different legal regimes. The principal official continues to accumulate credits within insulated institutional pension systems (such as the UNJSPF) or remains completely exempt from the Swiss social safety net. Conversely, the spouse’s Swiss payslip will show immediate, mandatory deductions for the Swiss first pillar—AVS (Age and Survivors' Insurance), AI (Invalidity Insurance), and APG (Loss of Earnings Allowance)—alongside compulsory enrollment in a local secondary pillar (LPP) managed by the employer's private pension fund. This creates a divided retirement portfolio where one partner builds a highly portable international pension, while the other locks capital into domestic Swiss structures bound by strict local withdrawal regulations.

The Health Insurance Threshold Trap

A common misconception among diplomatic circles involves mandatory health coverage under the Federal Health Insurance Act (LAMal). Legally, Permis Ci holders are technically exempt from mandatory Swiss LAMal if they remain covered by an equivalent institutional health plan (such as UNSMIS, CHI, or CERN health insurance). However, the hidden vulnerability lies within the internal statutes of the international organizations themselves:

-The Income Cap: Many institutional health funds automatically reclassify a spouse as a "secondary beneficiary" or terminate their coverage entirely if their local Swiss gross income crosses a specific internal threshold.

-The Forced Affiliation: If the spouse is disqualified from the institutional plan, they must immediately secure standard Swiss LAMal coverage within 90 days, exposing the household to premium domestic rates.

Strategic Conclusion

The decision to transition a diplomatic dependent into the Swiss domestic workforce requires a rigorous pre-contractual audit. Evaluating the exact net-income generation requires a precise calculation of global rate progression, Barème C exposure, local social security deductions, and institutional health fund caps. Utilizing specialized cross-border financial mapping frameworks is the only definitive method to ensure that spousal professional development within the Geneva district is executed as a strategic asset rather than an unmitigated administrative liability.