STATUTORY TAX ASYMMETRY AND THE RATE-DETERMINATION TRAP FOR MIXED-STATUS HOUSEHOLDS IN GENEVA

Legislative Foundations: The Friction Between Diplomatic Exemption and Joint Taxation

The arrival of international officials during the summer relocation cycle highlights a critical fiscal friction point in the Canton of Geneva: the tax status of mixed-status households. This scenario occurs when a primary official holds a diplomatic card (carte de légitimation type C or D, or an institutional card issued by the Federal Department of Foreign Affairs) while their spouse enters the local Swiss labor market via a Permis Ci or establishes an independent commercial practice.

This arrangement triggers a direct conflict between two distinct statutory frameworks:

-The Exemption Framework: Article 26 of the Federal Act on Direct Federal Taxation (LIFD) and Article 2 of the Host State Ordinance confirm that income derived from official mandates within international organizations (UN, WTO, WHO) or diplomatic missions is strictly exempt from Swiss income tax.

The Joint Taxation Framework: Article 9, Paragraph 1 of the LIFD and Article 4 of the Geneva Cantonal Law on the Taxation of Physical Persons (LIPP-V) dictate that married couples living in a shared household must be taxed jointly, blending their economic capacity into a single marital unit.

To reconcile these opposing statutes, the Swiss tax authorities utilize a mechanism known as Exemption with Rate-Determination (Exonération sous réserve de progressivité). Under this framework, the primary official's income remains non-taxable, but it is factorially integrated to determine the progressive tax bracket applied to the working spouse’s local income.

2. The Mechanics of Rate-Determination (Taux Global)

The Geneva Cantonal Tax Administration (Administration fiscale cantonale – AFC) does not assess the taxable spouse's income in isolation. Doing so would violate the constitutional principle of taxation according to economic capacity (Faculté contributive). Instead, the AFC establishes a theoretical combined worldwide income to determine the effective tax rate.

Case Simulation and Financial Breakdown

To evaluate the net financial impact of this structure, consider the following factual scenario:

The Primary Official: An international civil servant earning a net institutional salary of CHF 160,000 fully exempt from Swiss taxes under a valid headquarters agreement (Accord de siège).

The Spouse: A professional holding a Permis Ci, securing a position within a Geneva-based private firm with a taxable salary of CHF 80,000.

The Accounting Processing by the AFC:

Determination of Rate-Determining Income (Revenu déterminant le taux) : The AFC combines the exempt income and the taxable income ($160,000 + 80,000 = 240,000$).

Tax Bracket Selection: The AFC identifies the progressive tax rate applicable to a married household with a total income of CHF 240,000 under the joint splitting tariff (Tariff B).

Application of the Effective Rate: If the combined global rate for a CHF 240,000 baseline is evaluated at 22% (combining Cantonal, Communal, and Direct Federal taxes), this exact 22% rate is applied directly to the spouse's CHF 80,000 taxable income.

The Net Result:

Instead of being taxed at the standard rate for an isolated income of CHF 80,000 (which would yield an effective withholding tax rate of approximately 7% to 9% under standard marital splitting conditions), the spouse faces a final tax liability of CHF 17,600 ($80,000 $80,000 x 22).

This structural adjustment results in an immediate, non-refundable fiscal erosion of the secondary income, drastically lowering the household's projected net-of-tax cash flow.

3. The Quasi-Residency Bar: Post-2021 Withholding Tax Constraints

Following the comprehensive reform of the Swiss withholding tax system (Impôt à la source), which took effect on January 1, 2021, and is governed by Articles 99a and 115 of the LIFD, the administrative remedies for mixed-status households have become significantly restricted.

Historically, source-taxed individuals could file for regular corrections to claim specific deductions. Under the current legislative framework, a taxpayer subject to withholding tax can only access a Subsequent Ordinary Assessment (Taxation ordinaire ultérieure – TOU) if they qualify for Quasi-Resident Status.

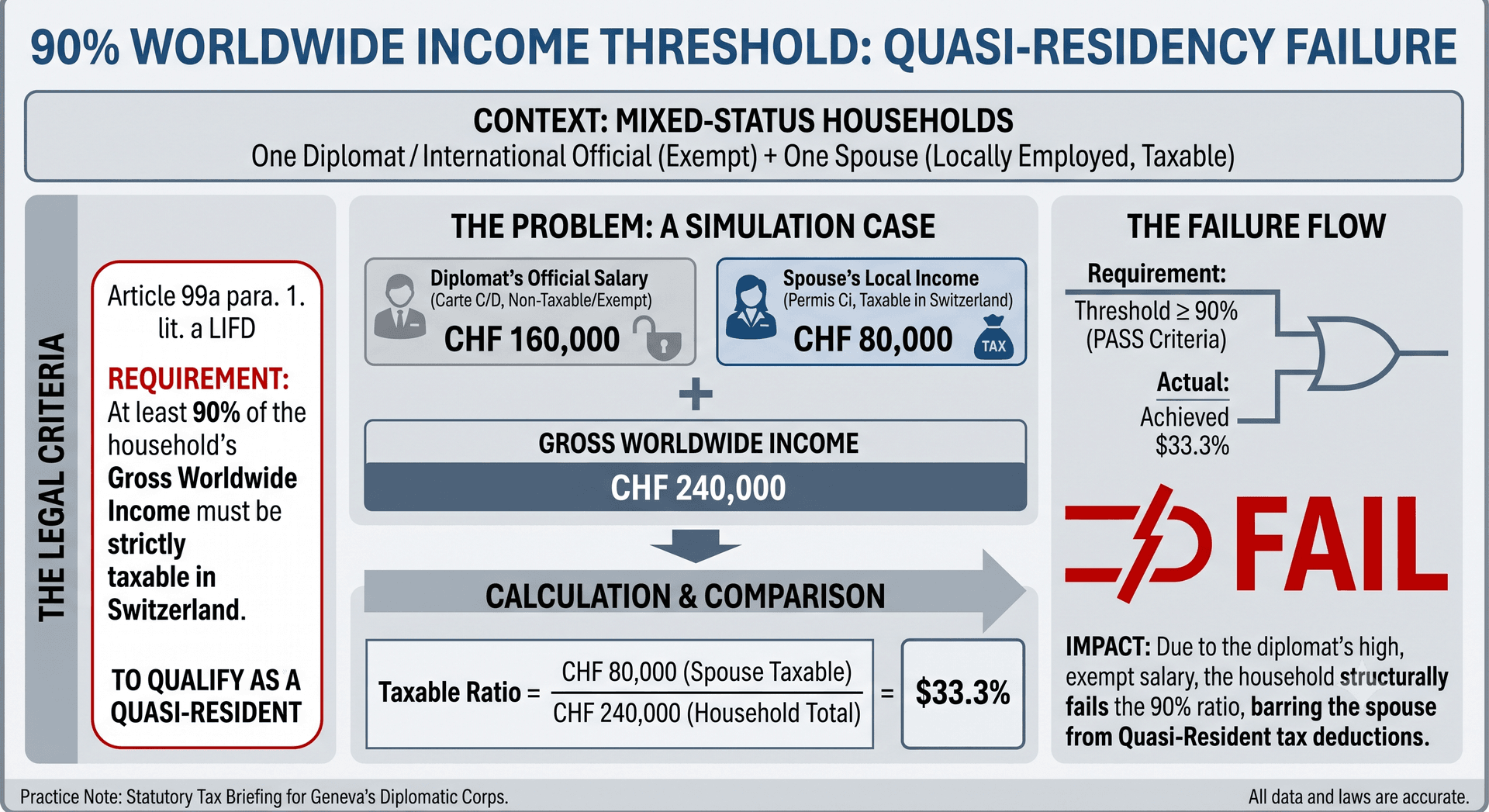

The 90% Worldwide Threshold Failure

To qualify as a Quasi-Resident in the Canton of Geneva, at least 90% of the household’s gross worldwide income during the tax year must be strictly taxable in Switzerland (Art. 99a para. 1 lit. a LIFD).

In a mixed-status household, this mathematical threshold is structurally impossible to achieve in nearly all cases:

Taxable Household Income Ratio Formula: Ratio = Spouse's Swiss Taxable Income ÷ (Diplomat's Exempt Income + Spouse's Swiss Taxable Income)

Applying the simulation data: Ratio = 80,000 ÷ (160,000 + 80,000) = 33.3%

Because the tax-exempt diplomatic salary represents 66.6% of the global household income, the taxable Swiss revenue fails to meet the 90% statutory requirement.

Loi fédérale sur l’impôt fédéral direct

The Structural Lock-In:

Consequently, the spouse holding the Permis Ci is legally barred from electing Quasi-Residency. This restriction means the household cannot file a retrospective tax return to claim critical deductions, including:

Contributions to individual voluntary pension schemes (Pillar 3a).

Actual professional or educational expenses exceeding standard flat-rate deductions.

International schooling fees for dependents or localized childcare costs.

The withholding tax applied under the global rate-determination framework becomes definitive and unadjustable, locking the household into a rigid tax structure.

4. Commercial Risk and Compliance for Spousal Corporate Vehicles

The fiscal challenges deepen if the spouse chooses to bypass traditional employment by establishing an independent practice, such as a Sole Proprietorship (Entreprise individuelle) or a Swiss Limited Liability Company (Sàrl).

THE COMPLIANCE CHAIN OF RISK

-Step 1: Corporate Inception – Spousal Commercial Enterprise (Sole Proprietorship or Sàrl) is established.

-Step 2: Revenue Generation – The entity generates localized corporate or independent commercial profit.

-Step 3: Audit Trigger – Local spousal profitability automatically initiates a joint cantonal tax audit of the shared household.

-Step 4: AFC Evaluation – The Cantonal Tax Administration (AFC) cross-references and assesses combined global household assets, including the primary diplomat's exempt revenue.

-Step 5: Structural Exposure – Risk of corporate asset reclassification and intense bank compliance friction under FINMA anti-money laundering guidelines.

Corporate Asset Segregation and Bank Compliance Friction

Under Article 10 of the LIPP-V, any localized business net profit generated by the spouse is fully taxable and subject to the rate-determination rules detailed above. However, the operational risk lies in asset classification.

Geneva commercial banks and compliance officers enforce strict anti-money laundering (AML) and source-of-funds protocols under the Swiss Financial Market Supervisory Authority (FINMA) guidelines. When a corporate entity or an independent account is tied to a household where the primary breadwinner enjoys diplomatic immunity, financial institutions require complete segregation of assets.

If corporate accounts are funded or collateralized using capital drawn from the primary official's tax-exempt, immune bank accounts, banks face significant regulatory hurdles. They may struggle to map the asset base cleanly for local corporate tax tracking.

This tension often triggers detailed cantonal audits to verify that the immune diplomat is not using the spouse’s local commercial vehicle to park or filter unmapped capital into the domestic economy. This scenario requires precise, proactive corporate bookkeeping and structured asset separation from day one. Mitigating the structural tax erosion inherent to mixed-status households requires proactive regulatory alignment before employment contracts are finalized or corporate structures are established. Contact our bureau to secure your household’s fiscal architecture and arrange a confidential statutory audit.