MEMORANDUM: 2026 VAT RECOVERY HARMONIZATION

Date: May 4, 2026

Status: Strategic Briefing for Financial Officers

The fiscal landscape of International Geneva has shifted. As of early 2026, the Swiss Federal Tax Administration (ESTV) has transitioned from a policy of "administrative tolerance" to one of strict algorithmic verification. For the institutional financial officer, this means that the "Safe Haven" status of a Mission or NGO no longer guarantees automatic recovery. Understanding the precise boundary between your diplomatic mandate and Swiss domestic tax law is now the difference between fiscal liquidity and a sequestered budget.

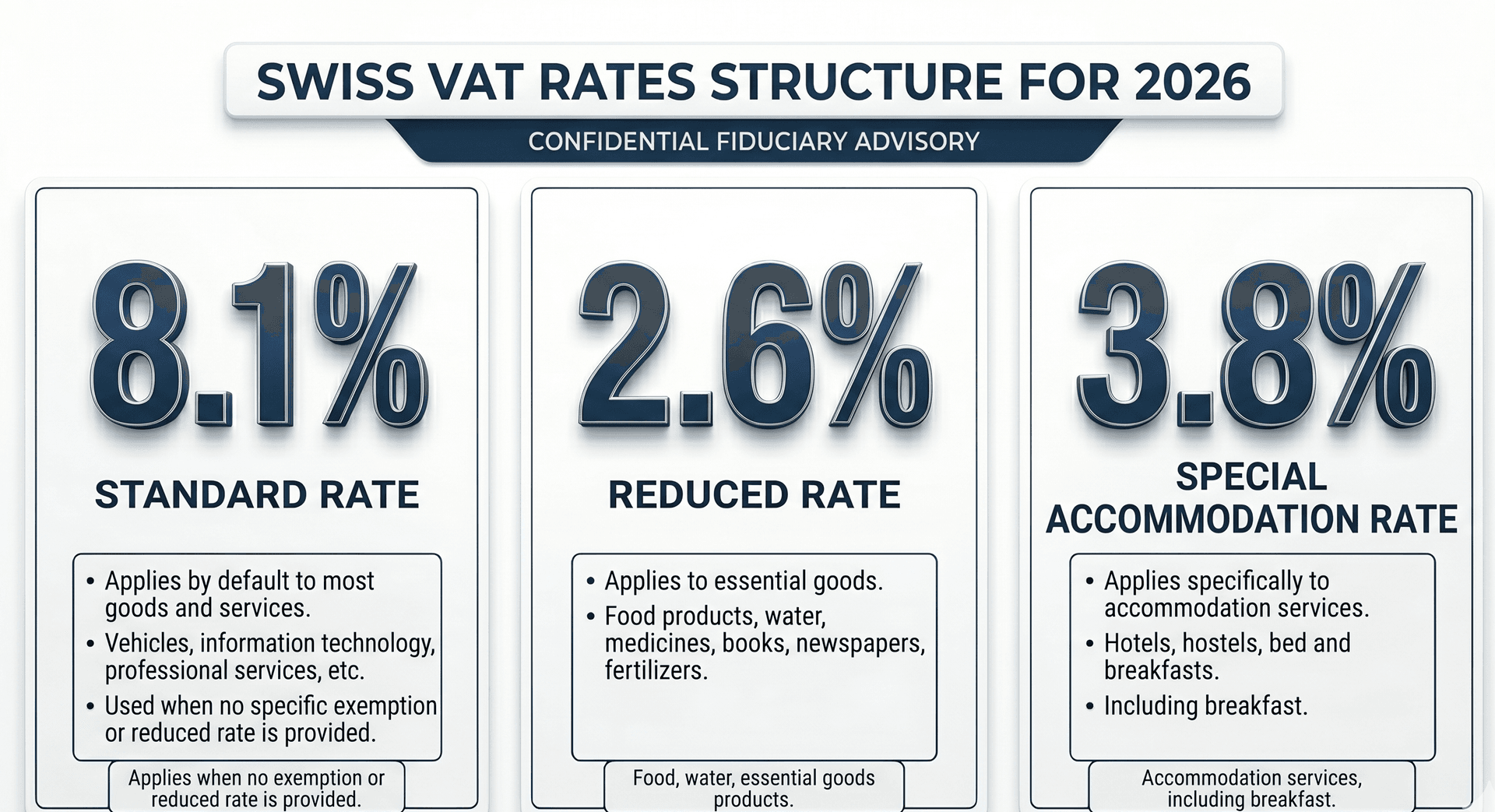

To navigate this, we must distinguish between the two primary tracks of recovery. Under the 2026 guidelines, Permanent Missions operate via the Sovereign Track (Art. 107 LTVA), which allows for a "Direct Exemption" on invoices over CHF 1,500 and a quarterly "Indirect Refund" for smaller amounts, provided each invoice is above CHF 100. Conversely, International NGOs utilize the Reciprocity Track (Form 1222), where they must pay the 8.1% VAT upfront and reclaim it annually; here, there is no per-invoice minimum, but the total claim must exceed CHF 500 per year.

The TARDOC Compliance Standard

The most significant hurdle this year is the full implementation of TARDOC (Tax Reporting and Documentation). Unlike previous years where a simple receipt might suffice, the ESTV’s automated 2026 audit systems now instantly reject any claim where the invoice does not perfectly match the federal registry.

Every document must now feature the supplier’s verified CHE-XXX.XXX.XXX VAT number and your organization's full official title. Even a minor discrepancy—such as using an abbreviation instead of the full registered name—triggers a "Hard Rejection." Our data indicates that since January, over 14% of submitted claims have been blocked due to these simple nomenclature errors.

Fiduciary Leakage and the "Audit of Intent"

"Fiduciary Leakage" is the primary threat to the 2026 budget. This occurs when fragmented invoices—those small, recurring costs for maintenance or services—are discarded because they fall below the CHF 100 threshold. However, the ESTV allows for Project Bundling. By grouping related service fees under a single contractual heading, a Mission can recover thousands of Francs that would otherwise be lost.

Furthermore, the "Audit of Intent" is now a standard part of the refund process. The ESTV is specifically looking for "Mixed-Use Capital." For example, if a Mission recovers VAT on a high-end vehicle fleet, but digital logs show use for non-accredited private purposes, the tax benefit can be revoked retroactively.

Securing Institutional Liquidity

Navigating these technical asymmetries requires more than bookkeeping; it requires forensic oversight. At Nouveau en Suisse, we act as the technical bridge, ensuring that every invoice is TARDOC-compliant from the moment it is issued. We transform the administrative burden of tax recovery into a streamlined workflow, ensuring that your capital remains under your control and your mandate remains fully funded.

Bureau of Institutional Advisory FINMA F01506548 | CICERO 43076 | nLPD Compliant